August 2025

SINGULAR

Fund Manager’s Report

From “Bye China” to “Buy China”?

[Drag image to zoom in]

But the mood has shifted. Shanghai- and Shenzhen-listed equities have started to outperform this month (CSI 300 +10.3%), prompting investors to ask whether it’s time to chase the rally. After all, major markets from the US to Japan have already hit record highs this year— could China be next?

Adding to the case, asset managers increasingly accept that ample liquidity will continue to fuel global equity gains. With China’s famously frugal households now dipping into their USD 23.0 trillion in savings and channelling funds into domestic stocks, the argument for joining the ride has grown stronger.

Still, plenty could go wrong. Asset managers were badly burned by Beijing’s heavy-handed crackdowns on tech giants and property developers in 2021. And the boom-and-bust cycle of 2015 remains a cautionary tale of just how unruly China’s retail-driven market can be. Yet despite these scars, investors are finding it harder to ignore the shifting incentives. With traditional income streams offering ever-thinner yields, the case for rebalancing toward equities has grown stronger.

Bond yields and bank deposit rates have trended lower, with one-year fixed deposits at China’s largest banks now paying just 0.95% annually—the lowest level on record. At the same time, authorities reinstated a 6% value-added tax on interest income from bonds issued after August 8, ending an exemption that had been in place since the 1990s. Together, these shifts are pushing investors to reassess their debt holdings and explore equities as a more attractive option.

The current rally shows both parallels and contrasts with earlier surges, notably in October 2024 and 2015. Average daily turnover in August 2025 hit a record RMB 2.2 trillion (USD 309 billion), surpassing the RMB 2 trillion peak of last October’s stimulus-driven boom. Retail participation has also surged, with new stock account openings in July up 71% year-on-year, but only about one-third of last October’s peak.

Compared with 2015, margin trading tells a more nuanced story. Outstanding margin balances have risen to RMB 2.28 trillion (USD 320 billion), slightly above the 2015 record. Yet China’s overall stock market has nearly doubled in size over the past decade. As a result, leveraged purchases account for 2.2% of market capitalization—just above the 10-year average, but far below the 2015 peak of 4.6%.

Nevertheless, signs of froth have prompted caution among financial institutions. Several brokerages and fund managers have scaled back financing and imposed purchase limits to temper momentum. One major Shanghai brokerage raised margin deposit ratios on selected securities, while some mutual funds capped daily inflows into their top-performing portfolios. Commercial banks, meanwhile, have tightened oversight by cracking down on clients using credit cards to fund stock trades.

[Drag image to zoom in]

Authorities also have a track record of stepping in when markets swing too far in either direction. Tools include restrictions on margin trading and short selling, as well as direct intervention by the “national team,” which can sell state holdings to signal intent and cool overheated rallies.

Looking ahead, stock selection will be critical. A sustainable rally is most likely to center on companies with the ability to consistently deliver profits, as well as emerging industries with strong growth potential.

Thailand: FDI Flows Defy Political Uncertainty

Yet, on the economic front, resilience remains evident. Foreign direct investment (FDI) has stayed robust: according to the Public Relations Department, applications for Board of Investment (BOI) incentives surged 132% year-on-year in the first half of 2025. Approved investment value reached USD 3.1 billion, a 37% increase over the same period last year. Key areas of inflow include the digital industry (notably data center services), contract manufacturing, and other high-value sectors, supported by various BOI incentives (see table below).

Some of the BOI Incentives

| Large Projects | Post-holiday 50% corporate income tax (CIT) reduction for 5 years for investments greater than or equal to THB 500 million. |

|---|---|

| Sectoral Incentives | Benefits for EV, semiconductors, biotech, and sustainability-focused projects. |

| Relocation Incentives | Tax holiday for setting up headquarters (HQ), R&D, and manufacturing in Thailand. |

| SME Upgrades | 5-year 100% CIT exemption for productivity investments. |

Source: Macquarie, BOI of Thailand

Discussions with major industrial land developers confirm this momentum, with land inquiries and transactions accelerating. Recent sales were quoted at around THB 5 million per rai (~RM39 per sq ft), representing a 25% increase from 2024 in comparable locations. Foreign investors are establishing increasingly automated manufacturing operations, reducing reliance on labour. Developers highlighted Thailand’s enduring appeal — competitive freehold land prices, attractive tax incentives within industrial estates, and reliable power and water supply. While political uncertainty persists, with the possibility of an election in the next six months, foreign investor appetite appears largely undeterred — may indicating that such risks have been internalised as part of the operating environment.

Emerging Themes from Macquarie’s 16th ASEAN Conference

Seatrium’s offshore shipyard in Tuas South

Looking back at the drivers, three policy signals stood out. First, Malaysia’s Minister of Investment, Trade and Industry set the tone with a framework of responsiveness, resilience and regionalism, highlighting trade diversification, fiscal reforms and closer ASEAN cooperation as anchors against tariff-related uncertainty. Second, Indonesia’s newly established sovereign fund Danantara confirmed its commitment to recycle Rp100 trillion of SOE dividends into both public and private markets, a clear signpost for long-duration domestic capital formation. Finally, Singapore’s Economic Development Board reinforced the Johor-Singapore Special Economic Zone as a centrepiece of supply-chain reconfiguration, targeting 100 projects in the next decade with early traction in logistics, healthcare and food manufacturing.

The Top 10 most requested corporates provided an interesting lens into investor sentiment. SEA and Grab dominated, as expected given their scale and headquarters in Singapore. But it was notable that high-performing small/mid-caps from the Philippines and Singapore also cracked the top tier, showing that investors are willing to look beyond the usual mega-cap tech names. Bank Mandiri and Astra International drew attention for Indonesia, while Gamuda from Malaysia saw strong demand on the back of its AI-driven data centre pipeline. The overarching tone was that while investors continue to prioritise “big platforms” for liquidity and scale, there is an emerging bid for regionally anchored companies with differentiated growth angles.

Sustainable Tropical Data Centre Testbed at NUS

The industrial tour highlighted Singapore’s dual role as a hub for advanced technology and consumer demand. Site visits included one of the world’s largest inland floating solar plants, Seatrium’s offshore shipyard in Tuas South, the Sustainable Tropical Data Centre Testbed at NUS, and the NUS CRISP satellite ground station—each underscoring Singapore’s push into renewables, digital infrastructure, and space technology. Complementing these, Keppel Infrastructure’s KI@Changi centre and SATS’ catering facilities illustrated the breadth of industrial capabilities across energy, logistics, and services.

Consumer and tourism takeaways were just as revealing. The Pop Mart Toy Fair that weekend drew extraordinary queues, with some reports noting lines stretching across multiple exhibition halls. Social media was flooded with photos of collectors waiting hours to enter, signalling not just strong retail demand but also the growing importance of “experience-led” consumption. The tourism-focused tour during the conference was oversubscribed, again reflecting the keen interest in Singapore’s ability to reinvent its consumer story even as

arrivals from China and Southeast Asia remain below pre-pandemic levels.

So the question becomes: if policy support is strengthening, corporates are signalling renewed investment intent, and global investors are returning to conference circuits in greater numbers, will foreign portfolio funds follow through with real capital flows into ASEAN markets?

Malaysia Market Review

Merdeka Momentum

[Drag image to zoom in]

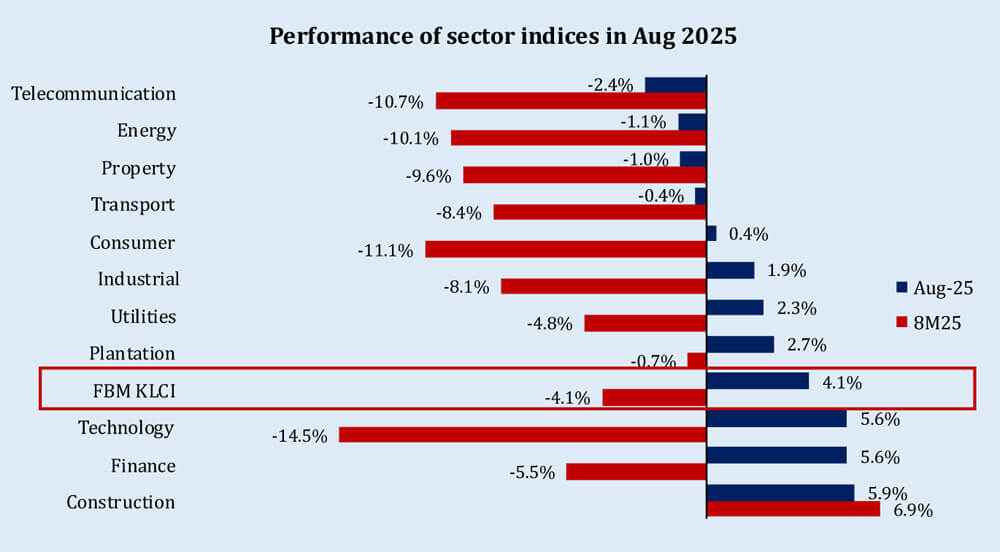

Earnings season ended slightly better than feared. Among 59 Malaysian companies under J.P. Morgan’s coverage, 27% beat and 47% met expectations. While FY25E EPS growth expectation was trimmed from 4.5% to 3.2%, the cuts were deemed shallow and narrow as 2H25 guidance seemed upbeat supported by liquidity and lower rates, along with some favourable shifts noted in August.

From a sector perspective, banks returned to the green in August, with the index up 5.6% MoM, its first positive month since Feb’25 driven by 2Q25 results that were broadly in line, which restored confidence after a soft 1Q. This drew local institutions back as banks made up RM1.0b of RM3.4b total net buys, making the sector the top purchase for the month. On fundamentals, cumulative loans growth moderated to 3.6% YoY as at end June’25 (from 4.4% at end of March), reflecting FX translation effects and still-cautious corporate sentiment. Net interest margins (NIMs) averaged 2.07%, down 2bps YoY but flat QoQ, as banks shed higher cost funding amid competitive pressure on asset yields. The slower loan growth and mild NIM compression were offset by stronger non-interest income (NOII) which grew 13.7% YoY and disciplined operating expenses that grew 3% YoY, lifting core net income growth by 3% YoY. Asset quality of banks also improved YoY, with absolute gross impaired loans (GILs) shrinking by 5% YoY, bringing overall GIL ratio down to 1.3% from 1.4%. Looking ahead, several banks have trimmed FY25E loan growth target to 5-6%, and revised NIM guidance lower by 5bps for the year, reflecting the impact of July’s OPR cut that will weigh on near-term margins. That said, management teams are deploying familiar mitigants—competing less aggressively in mortgages, optimising deposit mix to manage funding costs, and maintaining prudent credit standards. Together with manageable asset quality, should support earnings resilience and continue to position banks as stable holdings.

Following increased investments by global cloud and hyperscale operators, data-centre–led demand kept Malaysia’s industrial real estate firmly in focus—most visibly in Johor and Negeri Sembilan. According to the National Property Information Centre (NAPIC), overall property transaction volume slipped 1.3% YoY in 1H25, while the industrial segment remained resilient, with transaction volume up 8.5% YoY and value up 5.6% YoY to RM14.25b. This strength reflects a clear shift in capital allocation by land-rich owners—particularly plantation and property developers—who are increasingly repositioning under-utilised estates for industrial use. Coupled with constructive state-level support, the backdrop for better land utilisation and a multi-year industrial investment cycle is taking shape, with upside tied to the consistency of FDI demand.

本中文版由人工智能工具翻译,可能存在与英文版的差异。如有任何不一致之处,以英文版为准。

市场回顾

从“告别中国”到“买入中国”?

[Drag image to zoom in]

但如今,市场氛围已经转变。上海和深圳上市股票本月开始表现优异(沪深300指数 +10.3%),促使投资者思考:是否是追逐这一轮反弹的时机?毕竟,从美国到日本等主要市场今年都已创下新高——难道下一个会是中国?

进一步强化这一观点的是,资产管理人越来越接受充裕流动性将持续推动全球股市上涨。而中国素以节俭著称的家庭,如今也开始动用其23万亿美元的储蓄,将资金投入国内股市,使得“加入行情”的理由更具说服力。

然而,风险依旧存在。2021年,北京对科技巨头和房地产开发商的强力打压曾让资产管理人损失惨重。2015年的大起大落更是一个警示,揭示了中国散户主导的市场可能有多么难以驾驭。尽管这些伤痕尚存,但投资者越来越难以忽视激励结构的变化。随着传统收益渠道的回报日益稀薄,重新配置至股票的理由正在增强。

债券收益率和银行存款利率持续走低,中国大型银行的一年期定期存款利率已降至年化0.95%——创下历史新低。同时,监管部门恢复对8月8日之后发行的债券利息收入征收6%的增值税,终结了自上世纪90年代以来的免税待遇。这些变化共同推动投资者重新评估债务资产,转而将股票视为更具吸引力的选择。

当前这轮反弹既有与以往行情相似之处,也存在明显差异,尤其与2024年10月和2015年的行情对比鲜明。2025年8月的日均成交额达到创纪录的2.2万亿元人民币(3,090亿美元),超过去年10月在刺激政策推动下创下的2万亿元高点。散户参与度也在激增,7月新开股票账户同比增长71%,但仅为去年10月峰值的三分之一。

与2015年相比,融资融券的数据则呈现出更复杂的情况。融资余额已升至2.28万亿元人民币(3,200亿美元),略高于2015年的纪录。然而,中国股市在过去十年间几乎翻了一番。因此,融资买入占总市值的比重为2.2%——仅略高于十年均值,但远低于2015年的4.6%峰值。

尽管如此,市场泡沫迹象已促使金融机构保持谨慎。多家券商和基金公司缩减了融资规模,并对购买设限以抑制过快的势头。上海一家大型券商上调了部分证券的保证金比例,而一些公募基金则对其表现最佳的投资组合设定了每日申购上限。与此同时,商业银行也加强了监管,严厉打击客户利用信用卡资金进行股票交易的行为。

[Drag image to zoom in]

监管机构在市场波动过度时也有出手干预的先例。措施包括限制融资融券和卖空交易,以及由“国家队”直接入市,通过抛售国有持股来释放信号、降温过热行情。

展望未来,选股将成为关键。一轮可持续的上涨最有可能集中在那些具备持续盈利能力的企业,以及高成长潜力的新兴产业。

泰国:外资流入无惧政治不确定性

然而,在经济层面,韧性依然明显。外国直接投资(FDI)保持强劲:据公共关系部数据显示,2025年上半年投资促进委员会(BOI)激励措施的申请量同比激增132%。获批投资总额达31亿美元,比去年同期增长37%。主要流入领域包括数字产业(尤其是数据中心服务)、合同制造及其他高价值行业,并受到多项BOI优惠政策的支持(见下表)。与主要工业园区土地开发商的交流进一步印证了这一趋势,土地咨询与交易加速进行。近期成交价约为每莱500万泰铢(约合每平方英尺39令吉),与2024年相似地段相比上涨约25%。外国投资者正建立越来越自动化的制造运营,降低对劳动力的依赖。

Some of the BOI Incentives

| 大型项目 | 假期结束后,对投资额大于或等于5亿泰铢的项目,企业所得税(CIT)减半优惠为期5年。 |

|---|---|

| 行业激励 | 针对电动车、半导体、生物技术以及可持续发展相关项目的优惠政策。 |

| 搬迁激励 | 针对在泰国设立总部(HQ)、研发(R&D)及制造业务的投资,提供免税期。 |

| 中小企业升级 | 针对提高生产力的投资,给予5年100%企业所得税(CIT)豁免。 |

Source: Macquarie, BOI of Thailand

开发商强调了泰国持久的吸引力——工业园区内具有竞争力的永久产权土地价格、优厚的税收优惠,以及稳定的电力和供水。尽管政治不确定性依旧存在,并且未来六个月可能举行大选,但外国投资者的兴趣几乎未受影响——这或许表明此类风险已被视为经营环境的一部分并被内化。

麦格理第16届东盟会议的新兴主题

Seatrium’s offshore shipyard in Tuas South

回顾会议亮点,三大政策信号尤为突出。首先,马来西亚投资、贸易与工业部长提出“响应力、韧性与区域主义”的框架,强调贸易多元化、财政改革及更紧密的东盟合作,作为应对关税不确定性的支柱。其次,印尼新成立的主权基金 Danantara 确认将把1,000万亿印尼盾的国企分红循环投资于公私市场,明确表明其推动长期国内资本形成的决心。最后,新加坡经济发展局重申柔佛–新加坡特别经济区在供应链重组中的核心地位,目标在未来十年引入100个项目,目前已在物流、医疗与食品制造等领域初见成效。

最受投资者关注的十大企业也为市场情绪提供了有趣的视角。按预期,SEA与Grab凭借规模与新加坡总部优势位居前列。但值得注意的是,来自菲律宾与新加坡的部分高表现中小盘股也进入榜单,显示投资者愿意跳出传统的超大盘科技股范围。在印尼,曼迪利银行与阿斯特拉国际备受关注;而来自马来西亚的嘉马达则因其人工智能驱动的数据中心项目管线获得强劲需求。整体氛围是,投资者虽仍优先考虑具备流动性和规模的“大平台”,但对具备差异化增长路径、深植区域市场的公司兴趣正在上升。

Sustainable Tropical Data Centre Testbed at NUS

产业考察则凸显了新加坡在先进科技与消费需求上的双重角色。参观行程包括全球最大内陆漂浮光伏电站之一、位于大士南的Seatrium海上造船厂、国大可持续热带数据中心试验台,以及国大CRISP卫星地面站——均突显新加坡在可再生能源、数字基础设施及航天科技的布局。此外,吉宝基础设施的KI@樟宜中心与SATS的餐饮配套设施,也展示了涵盖能源、物流与服务领域的产业实力。

消费与旅游方面的观察同样令人印象深刻。会议期间举行的泡泡玛特玩具展吸引了长时间排队,部分报道甚至称队伍横跨多个展馆。社交媒体上充斥着收藏者等候数小时的照片,既体现了零售需求的旺盛,也反映了“体验式消费”的重要性日益上升。以旅游为主题的考察团同样爆满,再次说明即使来自中国和东南亚的游客数量尚未恢复至疫情前水平,新加坡依旧能够不断重塑消费故事。

因此,问题来了:在政策支持逐渐增强、企业释放再投资信号、全球投资者以更大规模回归会议场合的背景下,外国投资组合资金是否会真正跟进,把资本流入东盟市场?

马来西亚市场回顾

独立势能

[Drag image to zoom in]

财报季表现略好于预期。 在摩根大通覆盖的59 家马来西亚公司中,27%业绩超出预期,47%符合预期。尽管FY25E 每股盈利(EPS)增长预期从4.5%下调至3.2%,但下调幅度有限且集中,因为25 年下半年指引偏乐观,受到流动性和利率下行的支持,同时8 月也出现了一些有利变化。

从行业来看,银行股在8 月重返上涨区间,指数环比上涨5.6%,这是自2025 年2 月以来的首个正增长月。主要驱动因素是第二季度业绩大致符合预期,修复了一季度疲弱后的信心。这吸引本地机构资金回流,银行股净买入额达10 亿令吉,占当月净买入总额34 亿令吉的近三分之一,使其成为当月最受青睐的板块。基本面方面,截至2025 年6 月底,贷款总额同比增长3.6%(低于3 月末的4.4%),反映汇率折算效应和企业情绪依旧谨慎。净利差(NIMs)均值为2.07%,同比下降2 个基点,但环比持平,原因是银行在资产收益率竞争压力下逐步削减高成本资金。贷款增长放缓和净利差轻微收窄,被更强劲的非利息收入(NOII,同比增长13.7%)及3%同比增长的受控营运支出所抵消,使核心净利润同比增长3%。银行资产质量亦同比改善,不良贷款总额同比下降5%,整体不良贷款率(GIL)从1.4%降至1.3%。展望未来,多家银行已将FY25E 贷款增长目标下调至5–6%,并下调全年净利差指引5 个基点,反映7月降息对短期利差的影响。不过,管理层采取了熟悉的应对措施——减少按揭贷款领域的激烈竞争、优化存款结构以管理资金成本、并保持审慎信贷标准。结合可控的资产质量,应有助于支撑盈利韧性,使银行继续作为稳定的持仓。

随着全球云计算与超大规模运算企业增加投资,数据中心驱动的需求使马来西亚工业地产持续受到关注,尤以柔佛和森美兰最为显著。根据国家房地产信息中心(NAPIC)数据,2025年上半年整体房地产交易量同比下降1.3%,但工业地产板块保持韧性,交易量同比增长8.5%,交易金额同比增长5.6%至142.5亿令吉。这股力量反映了土地资源丰富的业主(尤其是种植园和地产开发商)的资本配置发生明显转变,他们正越来越多地将未充分利用的地块转向工业用途。加上州政府层面的积极支持,更好土地利用和多年工业投资周期的背景正在形成,而未来增长潜力取决于外资(FDI)需求的持续性。