April 2025

SINGULAR

Fund Manager’s Report

Trump’s Tariffs: Could The Bark Be Louder Than The Bite?

[Drag image to zoom in]

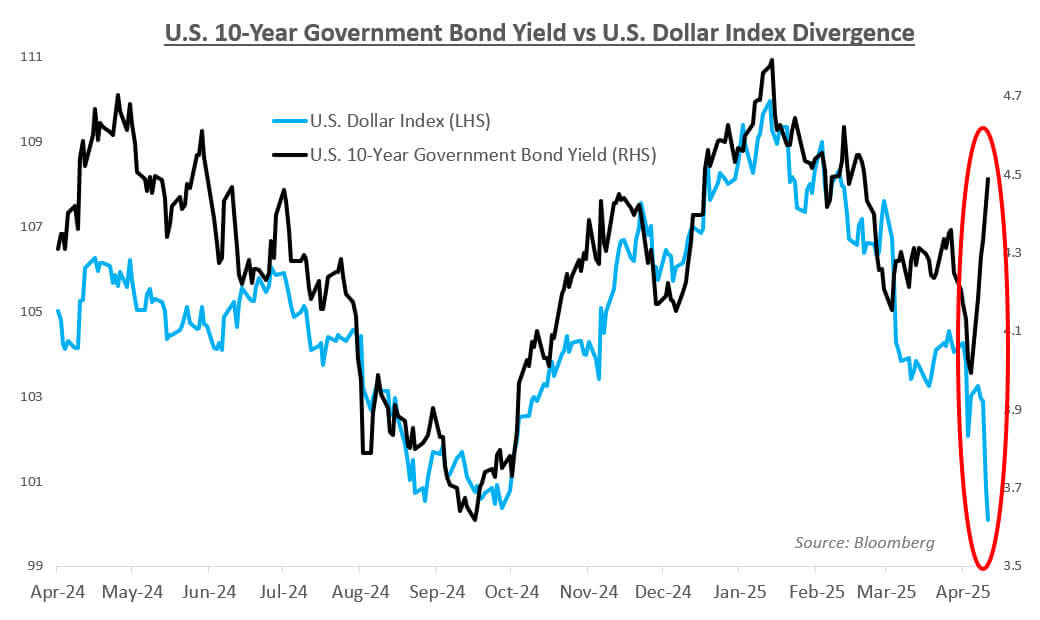

Back in 2018, tariff threats sparked familiar market reflexes: stocks sank, the dollar surged, and treasury yields dropped as investors fled to safety. Historically, during each of the last 18 corrections where the S&P 500 fell by 10% or more, the dollar strengthened as risk sentiment soured. This time, it fell. Bond yields, instead of retreating, edged higher. The inversion was striking. Are markets no longer treating the dollar as a safe haven?

[Drag image to zoom in]

In the U.S., consumers are starting to feel the pressure. Fast-fashion giant Shein, once celebrated for its rock-bottom prices, has raised prices by as much as 377% ahead of tariff increases. Retailers across sectors are warning of more to come if duties are enacted. The political cost is rising too. According to a mid-April CNN poll conducted just before the 100-day mark, Trump’s approval rating nationally fell to 41 percent. Campaign insiders reportedly talked him out of retracting his statement of wanting to fire Federal Reserve Chair Jerome Powell—worried that the move could amplify economic anxiety.

Hints of a climbdown are already visible. Exemptions are being granted—Apple, a major importer, appears to be off the hook, and other carve-outs may soon follow. While Trump continues to tout tariffs as a tool of strength, his tone has shifted. He has openly suggested that rates will come down from the initially floated 145% and, strikingly, offered a more conciliatory line on China. “We’re going to live together very happily and ideally work together,” he said, adding that he would be “very nice” to President Xi Jinping. The US administration’s moves seem to hint at a quiet recalibration. Could the final tariff package for majority of countries be lower than the headline figures announced in April?

What’s more telling is who isn’t reacting. Beijing’s moves seem calculated: no angry rebuttals, no urgent countermeasures. Instead, President Xi has been having high-profile meetings with Japan, South Korea, ASEAN leaders, building China’s diplomatic support. China, it seems, is choosing patience over panic—and this time, it may be doing so from a position of strength.

China - not flinching?

Some investors fear that Washington may try to tighten the screws through third-party channels, pressuring allies to limit Chinese imports. Mexico, for example, has reportedly considered stricter checks on selected Chinese goods. But the backlash isn’t universal. Japan, perceived as one of the US strongest ally, does not want to get caught up in any U.S. effort to maximise trade pressure on China by curbing its own economic interaction with Beijing, which is also Japan’s biggest trading partner and an important source of goods and raw materials – reaffirming its commitment to stable regional trade. Across ASEAN, China continues to engage diplomatically, with President Xi meeting regional leaders in a clear signal of economic alignment. Where the U.S. seeks to isolate China, many countries have kept quiet for now, signalling neutrality.

Meanwhile, the Chinese government continues to stand by its full-year GDP growth target of 5%, and early indicators offer some support. First quarter growth came in at 4.6%, and in March, retail sales rose 5.9% year-on-year, outpacing expectations. Categories such as home appliances and telecom products benefited from targeted support measures, while demand for staple food and sporting equipment surged 12% and 26% respectively. Though these figures predate the April tariff escalation, domestic economy seems to be holding its ground.

The auto sector offers another glimpse of China’s economic durability. Despite widespread discounting to clear legacy inventory in the first quarter, leading Chinese EV makers reported robust results. One major brand delivered over one million vehicles in 1Q25—a 60% year-on-year increase—while maintaining a healthy profit per car of around RMB8.7k. Lower average selling prices, driven by discounts on non-intelligent driving models, were more than offset by supply chain efficiencies and an improved product mix. Perhaps more significantly, 20% of those vehicles were exported—up from just 7% a year earlier. As global appetite for affordable EVs grows, China’s manufacturing scale and pricing flexibility are becoming strategic advantages.

[Drag image to zoom in]

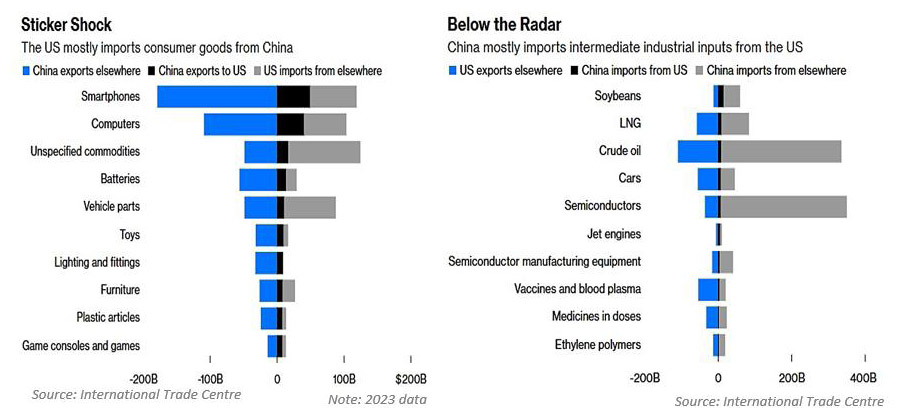

Trade data further underscores how China has “trade-proofed” itself. As shown in the charts above, only in the case of jet engines does China appear to rely heavily on U.S. suppliers. For most other key imports—such as semiconductors, LNG, and crude oil—China has developed a broad network of alternative trade partners. On the export side, the picture is even more resilient. China’s consumer goods, from smartphones to toys, are primarily sold to markets outside the U.S. Take smartphones, for instance: Observations from the chart above shows that the U.S. accounts for an estimated 20% of China’s smartphone exports, but those same imports make up roughly 30% of America’s total supply.

Is China’s silence a sign of confidence? Has China already done the hard work of de-risking its economy—diversifying supply chains, boosting domestic demand, and widening its trade footprint?

A settlement or a ‘deal’ between both parties will eventually come to fruition (in some form or another) – the questions is how long will this standoff last? A swift conclusion would undoubtedly be welcomed by equity markets, more crucially, help prevent further drag on an already fragile global economy. But if the dispute evolves into a prolonged, drawn-out affair, the consequences could be far more damaging. Global economy, the financial markets, would all feel the strain. The clock is ticking—and so is the cost of delay.

Singular Insights - China’s Electric Charge Faces New Crosswinds

China remains the undisputed global leader in electric mobility. Government support continues to fuel adoption—Jefferies estimates that trade-in and scrappage subsidies accounted for up to 70% of EV purchases in early 2025. CATL, the world’s largest battery maker, unveiled batteries capable of delivering 1,500km of range with charge times measured in minutes. Product innovation remains robust across the stack—from battery platforms to cabin automation.

Yet beneath the surface, competitive intensity has grown. We observed widespread price discounting, with transaction prices falling 10–20% year-on-year across many models. BYD’s Dynasty line, for example, has seen effective showroom prices drop more than 40% compared to two years ago. For many automakers, the focus is shifting from scale to survival.

To defend margins, Chinese EV makers are increasingly turning to overseas markets. In 2024, auto exports grew 23% year-on-year to more than 6.4 million units, making up roughly 20% of China’s total production. The largest destinations were Russia (~19%), Southeast Asia (~7%), and the European Union (~6%). While geopolitical risk remains (the EU imposed new tariffs in late 2024), most firms we met voiced confidence in the long-term export thesis—especially in markets where competition is less intense and ASPs are more defensible.

One flashpoint came in March, when a fatal crash involving Xiaomi’s SU7 sparked regulatory scrutiny on smart driving systems. Automakers have since pulled back on exaggerated autonomy claims. Xiaomi’s CEO Lei Jun notably skipped the Shanghai Auto Show entirely—a sharp contrast to his previous hands-on engagement. While the broader market impact appears contained, the episode served as a reminder: branding, safety, and consumer trust remain essential in premium positioning.

We left Shanghai with a sharper sense of both momentum and complexity in China’s EV landscape. Beneath the impressive technology and global ambitions lies a market adjusting to new realities—price pressure at home, political headwinds abroad, and a shifting narrative around what consumers value. It is not yet clear which companies will emerge stronger, or how the competitive field will evolve as regulation tightens and strategies mature. But the tone has changed. This is no longer just a race to scale—it is increasingly a test of focus, adaptability, and timing.

Malaysia Market Review

Tech Cycle: Boom, Bust…Reset?

Between late 2019 and early 2021, the tech index surged (+165%) on export-driven tailwinds and investor exuberance. That rally unravelled in 2022, when stretched valuations corrected sharply. While earnings held up initially, a delayed “catch-down” phase followed in 2023, pushing the current Price-to-Earnings (P/E) ratio back toward historic highs of 55x.

Fast forward to today: valuations now appear more palatable, with both current and forward P/E ratios settling below pre-pandemic levels—suggesting a more grounded investor sentiment. All told, it’s a sector reset that may warrant a closer look.

Silver Lining in Trade Clouds

For example, a local electronic manufacturing services (EMS) company shared that, despite earlier order holdbacks from a major customer exporting to the U.S. market, demand has since resumed and normalized following the tariff announcement in April. The company also secured new product wins expected to generate over RM800 million in additional revenue next year—underscoring the limited impact of tariff concerns.

Separately, a Penang-based equipment maker reported that its book-to-bill ratio has surged to 1.3x (approaching its 2021 peak), driven by a robust backlog across regions including ASEAN and North America amid ongoing global manufacturing realignments.

That said, part of the current momentum may reflect frontloading ahead of the U.S.’s 90-day reciprocal tariff suspension, which runs through July 8. As it stands, all countries except China are subject to a universal 10% tariff during this window. Unless a bilateral agreement is reached, Malaysia could face a 24% tariff thereafter—still among the lowest in the region. Another key event on the horizon is the AI diffusion rule, which is set to take effect on May 15, 2025.

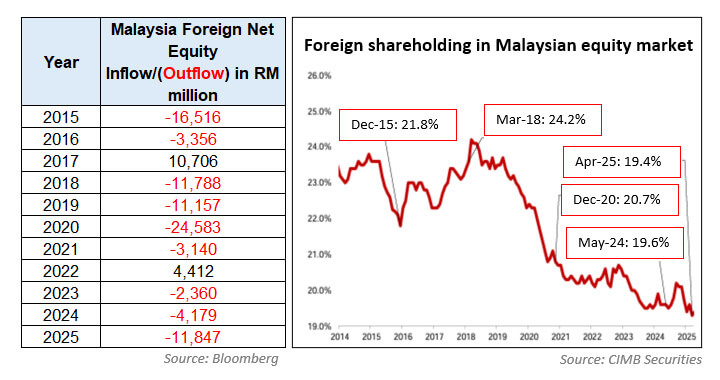

Foreign Exodus

[Drag image to zoom in]

Malaysia was not alone, however. Other regional markets also came under pressure, with Indonesia, in particular, registering even larger net outflows. On a more positive note, local institutions have stepped up as key buyers, helping to anchor the market and provide much-needed stability.

本中文版由人工智能工具翻译,可能存在与英文版的差异。如有任何不一致之处,以英文版为准。

特朗普的关税:叫声会比咬声更响亮吗?

[Drag image to zoom in]

早在 2018 年,关税威胁引发了熟悉的市场反射:股市下挫、美元飙升、国债收益率下跌,投资者纷纷逃往安全地带。从历史上看,在过去18次标准普尔500指数下跌10%或更多的调整中,每次美元都因风险情绪恶化而走强。这一次,美元下跌了。债券收益率非但没有回落,反而走高。这种反转令人震惊。难道市场不再将美元视为避风港?

[Drag image to zoom in]

在美国国内,消费者开始感受到压力。快时尚巨头Shein曾以其低廉的价格而闻名,但在关税上调之前,它已将价格提高了377%。各行各业的零售商都在警告说,如果关税实施,还会有更多的产品涨价。政治成本也在上升。根据美国有线电视新闻网(CNN)4 月中旬在 100 天大关前夕进行的民意调查,特朗普在全国的支持率降至 41%。据报道,竞选班子的内部人士劝说他不要收回想要解雇美联储主席杰罗姆-鲍威尔的声明,担心此举会加剧经济焦虑。

他的退让已显露端倪。苹果公司作为主要的进口商似乎获得了豁免,其他例外情况可能很快也会出现。虽然特朗普继续把关税作为一种强势工具,但他的语气已经发生了变化。他公开暗示,利率将从最初浮动的 145% 降下来,而且令人吃惊的是,他对中国提出了更加和解的路线。他说:“我们将非常愉快地生活在一起,最好能一起工作,”他还补充说,他会对习近平主席 “非常好”。美国政府的举动似乎暗示着一种悄然的重新调整。针对大多数国家的最终关税方案会低于四月份公布的标题数字吗?

更能说明问题的是谁没有做出反应。中国政府的举动似乎是经过深思熟虑的:没有愤怒的反驳,没有紧急的反制措施。相反,习主席一直在与日本、韩国和东盟领导人举行高规格会议,以建立中国的外交支持。看来,中国选择了耐心而非恐慌–而这一次,中国可能是站在实力的立场上这么做的。

中国--毫不退缩?

一些投资者担心,华盛顿可能会试图通过第三方渠道收紧银根,向盟国施压,限制中国的进口。例如,据报道墨西哥已考虑对部分中国商品实施更严格的检查。但这种反弹并不普遍。日本被认为是美国最强大的盟友之一,它不希望卷入美国的任何努力,即通过遏制自身与中国政府的经济互动来最大限度地对中国施加贸易压力,日本同时也是美国最大的贸易伙伴以及重要的商品和原材料来源国–日本重申了其对稳定地区贸易的承诺。在整个东盟,中国继续与东盟进行外交接触,习主席与地区领导人会晤,发出了经济结盟的明确信号。对于美国试图孤立中国的做法,许多国家暂时保持沉默,以示中立。

与此同时,中国政府继续坚持 5%的全年 GDP 增长目标,早期指标也提供了一些支持。第一季度增长率为 4.6%,3 月份零售额同比增长 5.9%,超出预期。家电和电信产品等类别受益于有针对性的支持措施,而主食和体育器材的需求则分别激增了 12% 和 26%。尽管这些数据是在 4 月份关税升级之前发布的,但国内经济似乎仍在坚守阵地。

汽车行业从另一个侧面反映了中国经济的持久性。尽管第一季度为清理遗留库存进行了大范围的打折促销,但中国领先的电动汽车制造商仍公布了强劲的业绩。一家主要品牌在 25 年第一季度的汽车交付量超过 100 万辆,同比增长 60%,同时保持了每辆车约 8.7 千元人民币的健康利润。供应链效率的提高和产品组合的改善抵消了非智能驾驶车型打折导致的平均售价下降。也许更重要的是,其中 20% 的汽车用于出口,而去年同期仅为 7%。随着全球对经济型电动汽车需求的增长,中国的生产规模和定价灵活性正成为其战略优势。

[Drag image to zoom in]

贸易数据进一步强调了中国是如何“对冲贸易风险”的。如上图所示,只有在喷气发动机方面,中国似乎仍高度依赖美国供应商。而在大多数其他关键进口品项方面——例如半导体、液化天然气(LNG)和原油——中国已建立起一个多元化的替代贸易伙伴网络。在出口方面,中国的韧性则更为显著。从智能手机到玩具等消费品,中国主要出口到美国以外的市场。以智能手机为例:从上述图表可观察到,美国大约占中国智能手机出口的20%,但这些进口却约占美国智能手机总供应量的30%。

中国的沉默是自信的表现吗?中国是否已经完成了消除经济风险的艰巨工作–实现供应链多元化、促进内需和扩大贸易足迹?

双方之间的和解或 “交易 ”最终会取得成果(以某种形式),问题是这种对峙会持续多久?迅速结束无疑会受到股市的欢迎,更重要的是,这将有助于防止进一步拖累本已脆弱的全球经济。但如果争端演变成一场旷日持久的旷日持久的事件,其后果可能更具破坏性。全球经济、金融市场都将感受到压力。时间在流逝,拖延的代价也在流逝。

鑫洞察 - 中国电动汽车充电面临新的挑战

中国仍然是电动汽车领域无可争议的全球领导者。政府的支持继续推动着电动汽车的普及–杰弗里估计,在2025年初,以旧换新和报废补贴占电动汽车购买量的70%。全球最大的电池制造商 CATL 推出了续航里程达 1,500 公里、充电时间仅需几分钟的电池。从电池平台到座舱自动化,产品创新依然强劲。

然而,在表象之下,竞争的激烈程度却有增无减。我们观察到广泛的价格折扣,许多车型的交易价格同比下降了 10%-20%。例如,比亚迪王朝系列的有效展厅价格与两年前相比下降了 40% 以上。对于许多汽车制造商来说,重点正在从规模转向生存。

为了保护利润,中国电动汽车制造商越来越多地转向海外市场。2024 年,汽车出口同比增长 23%,超过 640 万辆,约占中国总产量的 20%。最大的目的地是俄罗斯(约占 19%)、东南亚(约占 7%)和欧盟(约占 6%)。虽然地缘政治风险依然存在(欧盟于 2024 年底征收新关税),但我们遇到的大多数企业都表示对长期出口前景充满信心,尤其是在竞争不那么激烈、平均售价更有保障的市场。

今年 3 月,小米 SU7 发生致命车祸,引发了监管机构对智能驾驶系统的审查,这也成为一个热点。此后,汽车制造商们收回了夸大自动驾驶功能的说法。值得注意的是,小米公司首席执行官雷军完全没有参加上海车展–这与他以往的亲力亲为形成了鲜明对比。虽然对市场的影响似乎得到了控制,但这一事件提醒我们:品牌、安全和消费者信任对于高端定位仍然至关重要。

离开上海时,我们对中国电动车市场的发展势头和复杂性有了更清晰的认识。在令人印象深刻的技术和全球雄心的背后,是一个正在适应新现实的市场–国内的价格压力、国外的政治阻力,以及围绕消费者价值的不断变化的叙述。目前还不清楚哪家公司会更强大,也不清楚随着监管的收紧和战略的成熟,竞争环境将如何演变。但基调已经改变。这不再仅仅是一场规模竞赛,它越来越考验专注力、适应力和时机。

马来西亚市场回顾

技术周期:繁荣、萧条......重启?

2019 年底至 2021 年初,在出口驱动的顺风和投资者的热情推动下,科技股指数大涨(+165%)。这一涨势在 2022 年瓦解,估值急剧修正。虽然最初盈利有所增长,但 2023 年出现了延迟的 “追跌 ”阶段,将当前的市盈率推回到 55 倍的历史高位。

时至今日:现在的估值似乎更加合理,当前市盈率和远期市盈率都低于大流行前的水平,这表明投资者的情绪更加稳定。总之,这是一个值得仔细研究的行业重启。

贸易阴云中的一线希望

例如,一家本地电子制造服务(EMS)公司分享说,尽管早些时候一家出口美国市场的大客户搁置了订单,但在 4 月份宣布加征关税后,需求已经恢复并趋于正常。该公司还获得了新产品订单,预计明年将带来超过 8 亿令吉的额外收入,这表明关税问题的影响有限。

另外,一家总部位于槟城的设备制造商报告称,在全球制造业持续调整的背景下,东盟和北美等地区的强劲积压订单推动其账面订单比率飙升至1.3倍(接近2021年的峰值)。

尽管如此,目前的部分势头可能反映了在美国将于7月8日实施为期90天的互惠关税暂停之前的前置负荷。目前的情况是,除中国外,其他所有国家在这一窗口期都被普遍征收 10%的关税。除非达成双边协议,否则马来西亚此后将面临 24% 的关税–这仍然是该地区最低的关税之一。另一个即将发生的关键事件是人工智能扩散规则,该规则将于 2025 年 5 月 15 日生效。

外资大规模撤出

[Drag image to zoom in]

不过,马来西亚并非孤例,其他区域市场也面临同样压力,尤其是印尼,录得更大规模的资金流出。

值得庆幸的是,本地机构投资者挺身而出,成为主要买盘力量,在一定程度上稳定了市场情绪。