June 2025

SINGULAR

Fund Manager’s Report

Geopolitical Shockwaves Met with Market Resilience

[Drag image to zoom in]

While equities remained relatively stable, commodity markets told a different story. Brent crude spiked to as high as USD 78 per barrel, (~+20% from May). Although Iran accounts for only about 4% of global oil exports, the market’s primary concern centers on the Strait of Hormuz—a vital maritime choke point through which nearly 20% of the world’s oil flows each day. Any potential disruption in this corridor could severely impact global energy supplies and pricing. Yet, even amid these risks, markets have displayed a surprising degree of resilience.

Another noteworthy development is the continued decline of the U.S. dollar (see chart- DXY Index). This coincides with a noticeable shift in global capital flows. Based on EPFR data, both US domiciled US equity funds and overseas domiciled US equity funds posted outflows in June 2025. Similarly, data from LSEG Lipper concured with the net outflow of US equity funds. On the other hand, Hong Kong and China are attracting strong inflows, especially from domestic Chinese funds.

[Drag image to zoom in]

Beyond geopolitics, structural changes in China are drawing investor interest. Emerging consumer trends—such as a surge in spending on intellectual property-themed toys and heritage gold—and growth in sectors like biotechnology are capturing the attention of global capital.

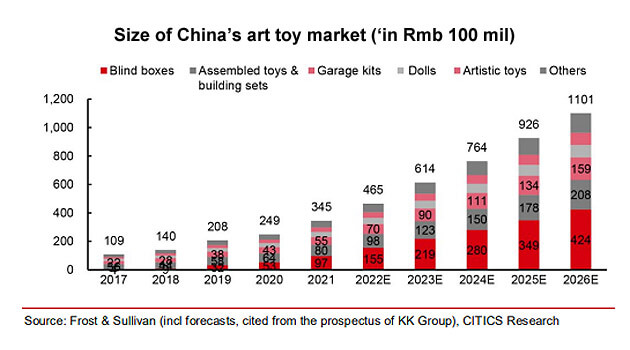

China’s Art Toys: Collectibles that Speak to a New Generation of Consumers

[Drag image to zoom in]

What leads the growth in this sector is the blind box model: consumers purchase sealed packages without knowing which character they contain. The allure lies in the chance of acquiring rare editions—driving both repeat purchases and an active secondary market.

The art toy phenomenon reflects a broader shift in Chinese consumer behaviour, especially among Gen Z (born 1995–2009). With China’s per capita GDP exceeding US$10,000 and urbanisation topping 60%, discretionary spending is tilting from functional goods towards “spiritual consumption” —products that deliver aesthetic, emotional or social value. For many in China’s increasingly single-person households, these toys also offer companionship and a sense of belonging through active online fan communities.

For firms, sustained success in the art toy space hinges on an IP strategy and creating characters that have strong emotional resonance with consumers. A long-lasting example of this is Hello Kitty and Disney characters. Now Chinese IP characters are entering the global stage such as Labubu and SkullPanda fuelled by the blind box model.

China is gaining ground in the global art toy market, raising the question of whether its IPs can achieve lasting global appeal like Hello Kitty or Disney, or if they remain short-lived trends. Beyond collectibles and blind boxes, the country’s biotech sector is also showing strong momentum. Together, these trends highlight China’s dual push to export both cultural influence and technological innovation.

Shanghai Biotech Insights: Global Partnerships Amid the Plum Rains

China’s oncology landscape is rapidly advancing—from chemical-based drugs, to targeted biologics, and now to antibody-drug conjugates (ADCs) that combine precision with cytotoxic potency. Duality Biologics exemplifies this leap, securing a GSK partnership with $30 million upfront and up to $1 billion in milestones.

Global pharma giants are deepening business development (BD) ties: AstraZeneca entered a $5.3 billion AI-enabled R&D deal with CSPC, while WuXi Biologics—now managing over 140 biologic projects annually—remains a top global CDMO. MicroPort MedBot, meanwhile, is disrupting surgical robotics with systems rivaling Intuitive Surgical’s Da Vinci at 30% lower cost.

Yet rising geopolitical scrutiny looms. The proposed U.S. Biosecure Act, which may restrict federal contracts with biotech firms linked to China, introduces new uncertainties. While partnerships persist, regulatory bifurcation could reshape global supply chains.

This raises a key investor dilemma: Can these companies sustain their global momentum amid geopolitical headwinds—and are the long-term rewards worth navigating the rising policy risks?

Malaysia Market Review

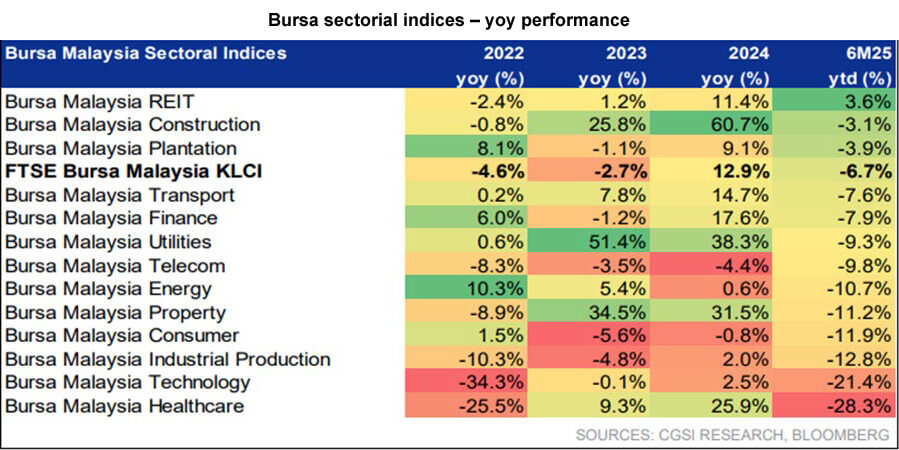

Malaysia 1H25 in Review: Reform and Resilience

[Drag image to zoom in]

From a currency-adjusted perspective, Malaysian equities remained relatively stable in 1H25, with returns down just -0.9% in USD terms, as losses were cushioned by a 6.2% appreciation in the ringgit against the greenback. Coincidentally, export-related sectors such as Healthcare (with gloves accounting for 17% of the Healthcare index’s market cap) and Technology were among the key laggards during the period.

On the flow front, foreign fund participation remained volatile. Net selling resurfaced in June, bringing year-to-date net outflows to RM 12.1billion (vs -RM 4.2 billion in 2024). Local funds, meanwhile, largely stayed on the sidelines. Cash holding ratios rose from 8.0% at the start of the year to 11.4% (according to JP Morgan’s estimate) – suggesting ample dry powder awaiting greater clarity. Further supporting domestic liquidity were the 15% year-on-year increase in EPF contributions in 1Q25 (to RM33.5 billion) and an additional estimated RM2 billion in contributions from foreign workers.

Since taking office, the MADANI government has rolled out a series of economic reform measures aimed at reducing subsidies and broadening the public revenue base; and it’s on track to reduce its fiscal deficit as % of GDP to 3.8% this year. These measures include the expansion of the Sales and Service Tax (SST), electricity tariff adjustments, and diesel subsidy rationalization — with RON95 remaining a potential next phase later this year. While these reforms are crucial for long-term fiscal sustainability, they may also lead to higher costs of doing business, though the impact is likely to vary across sectors.

Meanwhile, total approved investments reached record levels in 2024 and are projected to rise further to RM397 billion in 2025, with RM90 billion already recorded in 1Q25. Crucially, Malaysia is not only attracting capital — it is seeing those commitments translate into on-the-ground activity. This is most evident in Johor, which has emerged as a focal point for industrial and digital investment. The Johor–Singapore Special Economic Zone (JSSEZ), while still awaiting the release of its full blueprint in 3Q25, is already attracting strong cross-border interest. Notably, nearly 90% of Johor’s RM27.4 billion in new approved investments in 1Q25 were concentrated within the economic zone.

[Drag image to zoom in]

Further up north, our team conducted a three-day visit to Penang, meeting with ten companies across the technology supply chain. Overall, management teams were more optimistic on their 3Q25 outlook compared to the cautious tone in April and May. Order visibility is improving, and many expect 4Q25 guidance to firm up further after the finalization of the US tariff decision. Supply chain shifts remain in motion, with OSAT and EMS players positioning themselves to benefit as customers relocate operations from Vietnam, China, and Taiwan. Meanwhile, local equipment makers are expanding into high-growth segments such as AI, advanced packaging, and medical supplies.

Yet, the biggest overhang remains the 9 July US tariff decision. Until that fog lifts, Malaysia’s high export dependency — with exports accounting for roughly 70% of GDP — remains sensitive to any shifts in global trade policy.

本中文版由人工智能工具翻译,可能存在与英文版的差异。如有任何不一致之处,以英文版为准。

市场回顾

地缘政治冲击下的市场韧性

[Drag image to zoom in]

虽然股市相对稳定,但大宗商品市场却呈现不同景象。布伦特原油价格一度飙升至每桶78美元,较5月上涨约20%。尽管伊朗仅占全球原油出口的约4%,市场主要担忧的是霍尔木兹海峡——这是一个关键的海上咽喉,每天约有20%的全球原油经由此处运输。一旦该航道发生中断,可能会对全球能源供应和价格造成严重冲击。然而,即便在这一系列风险之中,市场整体依然展现出惊人的韧性。

另一个值得关注的是美元持续走弱(见图表——DXY指数)。这与全球资本流动的明显转变相吻合。根据EPFR的数据,2025年6月,美国本土的美股基金和海外设立的美股基金均出现资金流出。LSEG Lipper的数据也同样显示美股基金出现净流出。与此同时,香港和中国正吸引大量资金流入,尤其是来自中国本土基金的强劲流入。

[Drag image to zoom in]

除了地缘政治因素,中国的结构性变化也引发了投资者的关注。新兴消费趋势(如对IP主题玩具与传承黄金的消费热潮)以及生物科技等行业的发展,正成为全球资本瞩目的焦点。

中国艺术玩具:与新一代消费者对话的收藏品

[Drag image to zoom in]

推动该行业增长的关键模式是盲盒:消费者在不知情的情况下购买密封包装,无法预先得知其中是哪一款角色。其吸引力在于抽中稀有款的可能性——这不仅激发了消费者的重复购买,也催生了活跃的二级交易市场。

艺术玩具的流行反映出中国消费者行为的深层转变,尤其是在Z世代(1995年至2009年出生)群体中。随着中国人均GDP突破1万美元、城市化率超过60%,可支配收入的支出方向正从功能性商品转向“精神消费”——即具备审美、情感或社交价值的产品。对于中国日益增多的单人家庭而言,艺术玩具也在活跃的线上粉丝社群中提供了陪伴感与归属感。

对于企业而言,要在艺术玩具领域实现持续成功,关键在于构建IP战略,并打造能够引发消费者情感共鸣的角色。Hello Kitty和迪士尼角色便是历久弥新的典范。如今,在盲盒模式的推动下,中国原创IP角色如Labubu和SkullPanda也正逐步走向全球舞台。

中国在全球艺术玩具市场正不断取得进展,这也引发了一个问题:其IP能否如Hello Kitty或迪士尼一般,获得持久的全球吸引力,还是仅昙花一现?而在收藏品和盲盒之外,中国的生物科技产业也展现出强劲的发展势头。这些趋势共同体现了中国在文化输出与科技创新方面的双重发力。

上海生物科技洞察:梅雨季中的全球合作

中国的肿瘤治疗领域正经历重大变革:从传统化疗药物,到靶向生物药,如今迈入抗体药物偶联物(ADC)时代,兼具精准性与细胞毒杀伤力。映恩生物正是这一跃迁的典范,与葛兰素史克(GSK)签署合作协议,获得3000万美元预付款,潜在里程碑付款高达10亿美元。

全球制药巨头正加深业务发展(BD)合作:阿斯利康与石药集团达成53亿美元的AI驱动研发合作,药明生物则每年承接超过140个生物药项目,继续稳居全球领先的CDMO地位。与此同时,微创机器人则在手术机器人领域掀起变革,其系统可媲美直觉外科的达芬奇手术机器人(Intuitive Surgical’s Da Vinci),且成本低约30%。。

然而,地缘政治风险正在升温。美国拟议中的《生物安全法案》(Biosecure Act)可能限制与中国相关生物科技公司的联邦合约,带来了新的不确定性。尽管跨国合作仍在继续,但监管分化趋势或将重塑全球供应链格局。

这也引发了一个核心投资命题:在不断上升的政策风险下,这些中国生物科技公司能否维持其全球增长势头?而这种不确定性下的长期回报,是否值得投资者去拥抱?

马来西亚市场回顾

2025年上半年马来西亚回顾:改革与韧性

[Drag image to zoom in]

从汇率调整后的角度来看,2025年上半年马股相对保持稳定,以美元计回报仅下跌-0.9%,因令吉兑美元升值6.2%,有效缓冲了部分股市损失。巧合同时,以出口为导向的板块如医疗保健(手套占医疗保健指数市值的17%)和科技成为期间表现较弱的主要板块。

在资金流方面,外资参与度依然波动。净卖出情绪在6月再度浮现,使年初至今净流出扩大至121亿令吉(对比2024年为净流出42亿令吉)。与此同时,本地基金大多按兵不动。根据摩根大通的估算,现金持有比例从年初的8.0%上升至11.4%——显示市场中仍有大量观望中的“干火药”。支撑本地流动性的还有2025年第一季度雇员公积金(EPF)缴纳同比增长15%至335亿令吉,以及外籍劳工预计额外贡献的20亿令吉。

自上任以来,MADANI政府推出一系列经济改革措施,旨在减少补贴并扩大公共财政收入基础;财政赤字占GDP的比例预计将在今年降至3.8%。改革措施包括扩大销售与服务税(SST)覆盖范围、电费调整、柴油补贴合理化等——而RON95汽油或将在今年稍后成为下一阶段改革重点。尽管这些改革对财政的长期可持续性至关重要,但也可能导致企业营运成本上升,具体影响因行业而异。

与此同时,马来西亚在2024年实现了批准投资总额的历史新高,并预计将在2025年进一步增长至3970亿令吉,光是第一季度已录得900亿令吉。更重要的是,马来西亚不仅吸引到资本,更将其转化为实际的落地投资活动。这在柔佛表现尤为明显,该州已成为工业和数字投资的关键中心。尽管新山–新加坡特别经济区(JSSEZ)的完整蓝图仍预计在2025年第三季度公布,但已吸引到大量跨境关注。值得注意的是,柔佛在2025年第一季度获批的274亿令吉投资中,近90%集中在该经济区内。

[Drag image to zoom in]

往北看,我们团队进行了为期三天的槟城调研,拜访了十家科技供应链企业。整体而言,管理层对2025年第三季度的展望较4月和5月更为乐观。订单能见度有所改善,许多企业预计在美国关税决策最终敲定后,2025年第四季度的指引将进一步明确。供应链重组仍在持续,OSAT与EMS厂商正积极布局,以承接从越南、中国与台湾迁出的客户生产需求。同时,本地设备制造商也在进军如人工智能、先进封装和医疗器械等高成长领域。

然而,当前最大的不确定性依然是美国将于7月9日公布的关税决策。在这一不确定性消除前,马来西亚对出口的高度依赖——出口约占GDP的70%——将持续使其对全球贸易政策的变化保持高度敏感。