May 2025

SINGULAR

Fund Manager’s Report

Next Stop: Asia?

In early May, the Taiwan dollar surged nearly 6% against the U.S. dollar, marking its sharpest monthly rally since 1988 – driven by concentrated USD selling from exporters and insurers rebalancing hedges. Meanwhile, across the South China Sea, the Hong Kong Monetary Authority was forced to step into the currency market as the HKD touched the strong end of its trading band at 7.75 per USD — a level that triggered automatic intervention under the Linked Exchange Rate System.

[Drag image to zoom in]

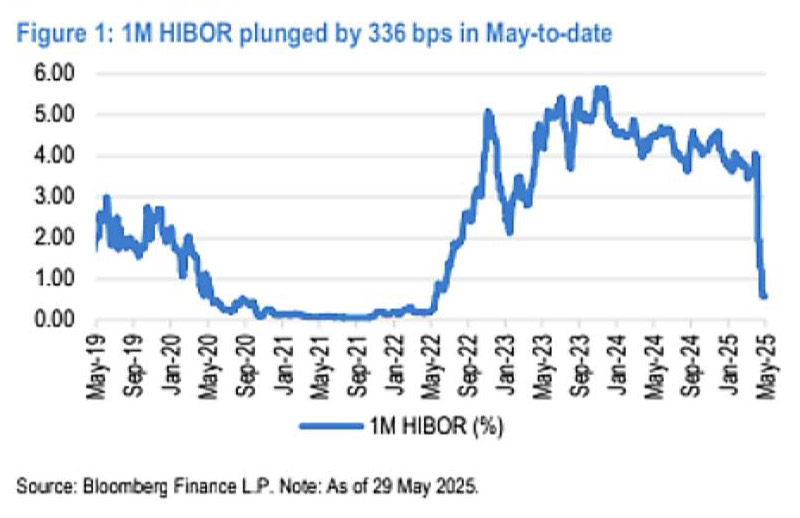

The Hong Kong Monetary Authority (HKMA) stepped into the market to sell HK$129.4 billion worth of local currency against the greenback in four intervention operations since Friday May 2, leading to the one-month Hong Kong Interbank Offered Rate declined 58 basis points to 3.08% on Wednesday, May 7, the most since 2008. Subsequently, as of 29th May 1M HIBOR plummeted by 335bps month-to-date (MTD) to 0.59%. A dramatic shift implying a sharp pullback in USD demand?

Adding to this is a fundamental rethink of U.S. fiscal sustainability. On May 16, 2025, Moody’s downgraded the long-term rating of the U.S. government from Aaa to Aa1, citing a decade-long trend of rising debt and interest burdens. The agency noted that “successive administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits,” and expects these imbalances to worsen.

The downgrade may trigger structural implications for global investors, particularly institutions that are restricted to holding only AAA-rated sovereign debt. The Hong Kong Mandatory Provident Fund Schemes Authority (MPFA) has already directed MPF trustees and fund managers to prepare contingency plans should the last remaining credit agency follow suit, potentially forcing sales of Treasuries from one of Asia’s largest retirement schemes. They are unlikely to be the only funds compelled to reduce exposure to U.S. Treasuries — a shift that would have been unthinkable just a few years ago.

So far, Europe has emerged as the primary beneficiary of this shift. In the week ending April 30th, European equity funds recorded $14.64 billion in inflows — the highest in over a year — while U.S. equity funds experienced outflows of $15.56 billion. The pivot marks a dramatic reversal from 2024, when European investors eagerly pursued high-performing U.S. technology stocks.

With Donald Trump again advocating a weaker dollar, and with a new proposal — Section 899 of his tax bill — threatening to impose punitive taxes on foreign investors from countries with so-called “discriminatory” tax regimes, the risks of weaponising U.S. capital markets are rising. Analysts warn that this move, which could raise federal income taxes by up to 20 percentage points on foreign-held passive U.S. income, may accelerate capital flight — especially among sovereign wealth funds, pensions, and institutional investors from countries like France, Canada, and Australia.

As global investors seek alternatives, could Asia be next in line to receive the world’s reallocated billions?

China Tourism – Prepare for take-off!

[Drag image to zoom in]

[Drag image to zoom in]

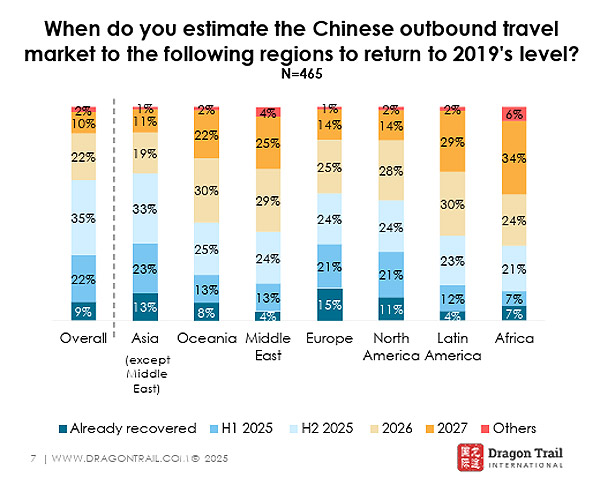

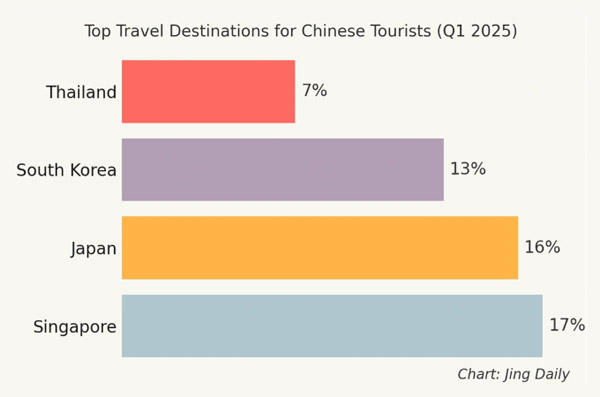

Destinations across Asia remain top choices—Singapore, Japan, and South Korea are clear favourites—while long-haul travel to Europe is gaining traction. Footfall from China to major European cities has soared, especially among affluent travellers drawn to cultural experiences and luxury shopping.

Domestically, tourism is equally vibrant. The government is doubling down on expanding cultural and tourism events to fuel domestic consumption. Improved transport infrastructure—particularly new airports and high-speed rail lines—has unlocked access to lower-tier cities, now emerging as popular weekend escapes. The rise of “micro-vacations” is being catalysed by local initiatives like the 4.5-day workweek, piloted in cities such as Chongqing, turning short getaways into a new form of luxury.

On the inbound front, China is becoming increasingly attractive to international visitors. A wave of favourable policy shifts—such as visa-free transit expansions and a streamlined nationwide instant tax refund system—is lowering travel friction. As one returning American visitor noted, “The last time I came seven years ago, the tax refund process was tedious. This time, the instant refund made shopping a breeze.”

Since late 2024, China has significantly broadened its visa-free access. In November, nine more countries were added to its visa waiver list. By year-end, the visa-free transit window had been extended to 240 hours (10 days) from 72 hours initially, with 60 (from 39) designated entry-exit ports. China had also signed mutual visa exemption agreements with 25 countries (26 if Uzbekistan is included, effective from June 1, 2025) and offered unilateral visa-free entry to citizens from 38 nations (43 if including Brazil, Argentina, Chile, Peru and Uruguay).

Momentum is clearly building. Interest in visiting China is surging across global social platforms, with hashtags like #ChinaTravel trending consistently. The surge is translating into spending: during the first three days of the May Day holiday, Alipay reported that international tourist spending in China jumped 180% year-on-year.

Singular Insight – “Sole”-searching

Unlike recent years, we observed a notable increase in interest from foreign investors. Fund managers from Europe, India, and Southeast Asia were present.

Our discussions with corporate management confirmed this trend, as many noted the growing attention from international funds. In particular, large Hong Kong-listed companies have packed schedules over the coming weeks, with strong demand for meetings and multiple brokers inviting them to conferences, reflecting the renewed interest in Chinese corporates.

In terms of corporate engagement, the main topics of discussion were the impact of U.S. tariffs and domestic demand trends. Shoe manufacturers shared that most international sportswear brands are currently absorbing the 10% U.S. tariff. Many of these manufacturers have diversified their production to Southeast Asia, including countries like Vietnam and Indonesia. One producer mentioned that manufacturing costs in alternative locations such as Italy or Mexico are at least three times higher. Due to Chinese manufacturers’ experience, cost efficiency, and established overseas facilities, it remains challenging for brand owners to shift production entirely to other region.

Malaysia Market Review

May-day for corporate results?

[Drag image to zoom in]

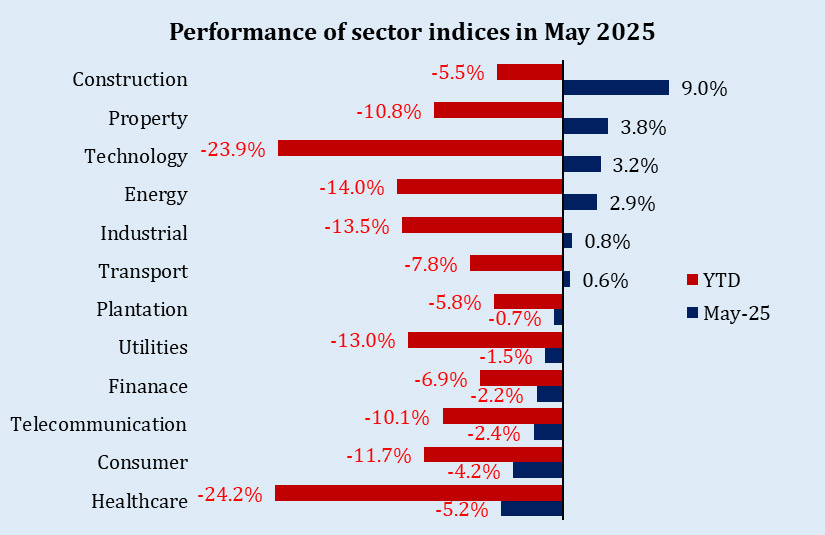

Beneath the benchmark’s lacklustre performance (FBM KLCI -2.1%) this month, sector rotation gained pace: consumer stocks consolidated after a strong April, while AI/data centre names rallied on the rollback of Biden-era AI export rules. Still, the FBM KLCI (-8.2% YTD) is on track for its weakest first half in recent years, following a solid performance last year. More notably, broader market breadth remains thin, with over 79% of the 1,018 traded stocks on the local bourse ending in the red year-to-date.

Flow wise, May marked a tentative turning point. Foreign investors turned net buyers by accumulating RM 1.0 billion in equities – the first monthly net inflow after a prolonged stretch of selling.

Turning to the corporate front, the recent earnings season ended on a subdued note. Based on a basket of 57 companies tracked by JP Morgan, only 21% beat expectations, 48% met them, and the remainder fell short—with notable earnings misses in the glove and auto sectors. As a result, consensus forecasts for KLCI earnings growth in FY25 have also been revised down to 5%, from earlier estimates of 9%.

Kicking off with the banks, several results came in below expectations. Cumulative loan growth eased to 4.4% YoY as of end-Mar 2025 (from 5.5% in Dec), while net interest margins (NIMs) slipped by an average of 2bps QoQ —though they generally remained within their respective FY25 targets. With lower Non-Interest Operating Income (NOII) and negative JAWS, core operating profit rose just 1% YoY. Nonetheless, core net profit rose 4% YoY, aided by lower credit costs. Meanwhile direct exposure to US tariff-sensitive loans remained minimal (less than 4%), but banks noted weaker trade-linked demand and deferred capex, prompting one lender to cut loan growth guidance to 5–6%. Looking ahead, changes to the Statutory Reserve Requirement (SRR) may offer a modest boost to margins, though potential rate cuts remain a risk.

For Telcos, while reported results met expectations, topline growth remained modest and profitability came under pressure. Both mobile and fixed broadband segments recorded stable subscriber growth, but ARPU (average revenue per user) declined across the board amid heightened competition and the increasing prevalence of convergence strategies. Fixed broadband subscriber growth continued to be supported by wider fibre coverage and increased adoption of bundled offerings, though ARPU fell due to promotional pricing and device subsidies to attract and retain customers. Mobile performance mirrored this, with stable subscriber bases offset by softer pricing dynamics due to competitive pressure. Looking ahead, Telco operators maintained conservative guidance while anticipating stronger contributions from convergence and enterprise segments.

Contrary to the broader market’s lacklustre earnings, leading contractors delivered strong results this quarter as revenue recognition gained momentum from ongoing chunky jobs begun to filter through. Margins also improved, supported by falling input costs—particularly steel rebars, which dropped 14% to RM2,400/ton in May from RM2,800 in November. However, this sharp correction took a toll on local steelmakers, many of whom reported losses. With Chinese rebar selling at just RM1,800/ton—around 75% of local prices—the resulting overhang may continue to pressure the domestic steel industry.

Looking ahead, leading contractors continue to guide for order book expansion, with rising tenders increasingly driven by private-sector projects. While data centre jobs dominate among large players, high-rise residential and commercial projects are beginning to feature heavily in small and mid-cap contractors’ books. Management teams hint at more job awards ahead as clients firm up the specs and approvals.

本中文版由人工智能工具翻译,可能存在与英文版的差异。如有任何不一致之处,以英文版为准。

下一站:亚洲?

2025年5月初,新台币兑美元汇率飙升近6%,创下自1988年以来的最大单月涨幅,主要受到出口商与保险机构集中抛售美元、重新平衡对冲头寸的推动。与此同时,在南中国海彼岸,港元兑美元汇率触及7.75的强方兑换保证区间,触发了联系汇率制度下的自动干预机制,香港金融管理局(HKMA)被迫多次入市干预。

[Drag image to zoom in]

自5月2日(周五)起至今,金管局已在市场上进行了四次干预操作,累计沽出港元1,294亿以捍卫联系汇率制度。这导致一个月期香港银行间拆借利率(HIBOR)在5月7日大跌58个基点至3.08%,为2008年以来最大单日跌幅。此后,截至5月29日,1个月期HIBOR月内累计下跌335个基点至0.59%。这一剧烈变动或反映出美元需求的明显回落。

与此同时,美国财政可持续性也遭遇根本性质疑。2025年5月16日,穆迪将美国政府的长期信用评级从Aaa下调至Aa1,理由是债务水平和利息负担在过去十年持续攀升。穆迪指出,“历届政府和国会均未能就遏制巨额年度财政赤字的举措达成一致”,预计未来财政失衡情况还将加剧。

这一评级下调可能对全球投资者带来结构性影响,尤其是那些受限于只能持有AAA评级主权债券的机构投资者。香港强积金管理局(MPFA)已指示受托人和基金经理制定应急方案,以应对最后一家评级机构若也跟随下调所引发的潜在美债抛售潮。强积金可能只是第一批被迫减持美国国债的机构之一,这在几年前还是难以想象的场景。

目前来看,欧洲是这场资本重配的主要受益者。截至4月30日当周,欧洲股票基金录得146.4亿美元净流入,创一年多来新高;而美国股票基金同期则遭遇155.6亿美元资金净流出。这标志着相较2024年的局面发生了戏剧性的反转,当时欧洲投资者还在追捧表现亮眼的美国科技股。

随着唐纳德·特朗普再次主张“弱美元”政策,并提出新的税改条款——其税案中的第899条款计划对来自“歧视性”税收制度国家的外国投资者征收惩罚性税收——美国资本市场被“武器化”的风险正在上升。分析人士警告称,该提议可能会将外国持有的美国被动收入的联邦所得税税率提高多达20个百分点,进而加速资本外流,尤其是来自法国、加拿大和澳大利亚等国家的主权财富基金、养老金与机构投资者。

在全球资金寻求替代资产的过程中,亚洲是否将成为下一个承接数千亿美元资本重配的热土?

中国旅游 - 准备起飞!

[Drag image to zoom in]

[Drag image to zoom in]

亚洲各地仍是中国游客的首选目的地——新加坡、日本和韩国位居前列;而远程赴欧旅游也正在升温,前往欧洲主要城市的中国游客数量激增,尤其是那些追求文化体验与奢华购物的高净值人群。

在国内旅游方面,热度同样不减。中国政府正加码推出各类文化与旅游活动以提振内需。交通基础设施的持续完善——尤其是新建机场与高铁线路的铺设——已打通通往低线城市的通道,使其逐渐成为热门周末度假目的地。“微度假”的兴起,受到如重庆等地试点的“4.5天工作制”等地方政策的推动,短途旅行正在演变为一种新的“轻奢”。

在入境旅游方面,中国对国际旅客的吸引力也在持续上升。一系列利好政策的推出——如扩大免签过境范围、全国范围内实施即时退税系统——有效降低了出行门槛。一位重访中国的美国游客感慨道:“我七年前来的时候,退税流程相当繁琐;这次,即时退税让购物轻松愉快。”

自2024年底以来,中国大幅扩展了免签政策。去年11月,又有9个国家被纳入免签名单。截至年末,免签过境停留时间从最初的72小时延长至240小时(10天),指定口岸数量也从39个增至60个。此外,中国已与25个国家(若将乌兹别克斯坦纳入,则为26个,生效日为2025年6月1日)签署了互免签证协议,并对来自38个国家的公民实施单方面免签(若将巴西、阿根廷、智利、秘鲁和乌拉圭算入,则为43个国家)。

这一趋势正在形成强劲势能。全球社交平台上,“#ChinaTravel”等标签持续走红,显示出游客兴趣的快速升温,并逐渐转化为实际消费行为。以“五一”假期为例,支付宝数据显示,假期前3天国际游客在华消费同比激增180%。

鞋底之下,(鑫)洞察之上

与近年来的情况不同,我们明显感受到海外投资者兴趣的回暖。来自欧洲、印度及东南亚的基金经理纷纷到场。

我们与企业管理层的交流也印证了这一趋势,许多公司提到,近期收到越来越多来自国际基金的关注。尤其是大型香港上市公司,未来几周的行程已排得满满当当,不仅会议需求强劲,还有多家券商邀请出席投资会议,反映出海外资金对中国企业兴趣重燃。

在企业交流方面,讨论的核心话题主要集中在美国关税影响及国内消费需求趋势。鞋厂普遍反映,目前多数国际运动品牌仍在自行吸收10%的美方加征关税。许多企业已将部分产能多元化布局至东南亚,例如越南和印尼。其中一位厂商指出,若将生产转至意大利或墨西哥,制造成本至少高出三倍。受益于中国制造商在经验、成本效率及海外产能上的优势,品牌方目前仍难以完全将供应链转移至其他地区。

马来西亚市场回顾

企业财报,五月遇“危”?

[Drag image to zoom in]

尽管大盘表现乏力(FBM KLCI本月下跌2.1%),板块轮动步伐却明显加快:消费股在经历4月强势上涨后出现整固,AI及数据中心概念股则因拜登时期AI出口管制政策的部分回撤而上涨。不过,FBM KLCI年初至今仍下跌8.2%,可能录得近年来相对逊色的上半年表现。更值得注意的是,市场广度依旧偏弱,截至目前,马股市场上1,018只活跃交易股票中,有超过79%录得年内跌幅。

从资金流向看,5月或成为一个初步转折点。外资在连续多月净卖出后,转为净买入马股股票,录得净流入10亿令吉,为今年首个单月正流入。

企业方面,最新一季财报季整体表现温和。根据摩根大通追踪的57家样本公司,仅21%的业绩超出预期,48%符合预期,其余则逊色——其中手套与汽车板块的盈利低于预期较为明显。因此,市场普遍下调对FBM KLCI 2025财年的盈利增长预测,从原先的9%下修至5%。

银行股方面,多家银行业绩未达预期。截至2025年3月底,整体贷款同比增速放缓至4.4%(去年底为5.5%),净息差(NIM)平均季度环比下降2个基点,虽仍处于全年指引区间。受非利息收入下降及负向 “JAWS” 效应影响,核心营业利润同比仅增长1%,但在信贷成本下降的支撑下,核心净利润同比增长4%。虽然对美方关税相关贷款的直接敞口不足4%,但银行普遍反映,贸易相关融资需求疲软,企业延后资本支出,导致部分银行将全年贷款增长指引下调至5–6%。展望未来,法定储备金率(SRR)调整有望带来一定息差提振,但潜在降息风险仍不容忽视。

电信板块方面,尽管整体财报符合市场预期,营收增幅仍属温和,盈利能力面临压力。移动与固网宽带用户增长保持稳定,但受竞争加剧与融合策略影响,ARPU (每用户平均收入) 普遍下滑。固网宽带受益于光纤覆盖扩大与捆绑产品普及,用户增长良好,但因促销定价与设备补贴,ARPU承压。移动业务亦呈现类似趋势,用户规模稳定但定价趋软。展望下半年,运营商维持审慎指引,预计融合与企业业务将成为增长主要驱动。

与整体市场偏弱的盈利表现不同,建筑主承包商本季业绩亮眼,主要受大型在建项目收入确认加快带动。利润率也同步改善,受益于原材料成本下滑,尤其是钢筋价格自2024年11月的RM2,800/吨下跌14%至2025年5月的RM2,400/吨。然而,钢价回调对本地钢铁业者形成巨大冲击,不少公司录得亏损。与此同时,中国钢筋价格仅RM1,800/吨,仅为本地价格的75%左右,这一价差将持续对本地钢铁行业构成压力。

展望未来,领先承包商普遍指引订单簿仍具扩张潜力,私营项目成为近期标案主力。大型承包商以数据中心项目为主导,小中型业者则逐渐接获更多高楼住宅与商业建筑项目。多家管理层透露,随着客户技术规范与审批逐步落地,未来将有更多项目进入授标阶段。