September 2025

SINGULAR

Fund Manager’s Report

China’s Rally: Just the Start, and Can It Be Sustained?

[Drag image to zoom in]

Falling interest rates are an important backdrop. One-year bank deposit yields now sit below 1%, the lowest on record, pushing households to consider alternatives. With cash returns compressed, equities are gaining relative appeal in the search for yield.

Domestically, state-linked institutions are anchoring the market. Central Huijin, part of China Investment Corp., has built up about USD 180 billion in ETFs, generating sizeable paper gains as markets rallied. Large insurers have been directed to allocate 30% of new policy premiums into equities, ensuring a stable base of institutional demand.

Foreign investors are also returning. Bloomberg recently reported that China is shedding the “uninvestable” label, with global funds stepping back in across multiple asset classes for the first time since 2021. Hedge funds were particularly active in A-shares, while long-only managers have begun adding exposure. At the same time, interest in Hong Kong’s IPO market is reviving, providing another channel for international capital to engage with China.

While domestic and regional funds have been quicker to rotate into Chinese and Hong Kong equities, global investors have yet to return in full strength. Positioning data show that Asian and EM-focused funds have been steadily increasing their China allocations this year, while global active managers remain underweight relative to benchmarks. This gap highlights that much of the recent rally has been driven by regional flows, leaving scope for further upside should global funds decide to re-engage more decisively.

In Hong Kong, IPO fundraising is staging a comeback. In the first half of 2025, 42 new listings raised HKD 107.1 billion, a more than 700% increase compared with the prior year. Average aftermarket performance has also been positive, helping restore confidence in the city’s role as a gateway for global capital into China.

Corporate fundamentals seem to be nudging upward in certain pockets. Utilisation rates and average selling prices are trending higher, helped by Beijing’s “anti-involution” campaign that is encouraging more rational competition. Earnings in listed companies improved in the first half, with consensus forecasting mid-single-digit growth this year and a compound annual growth rate of around 9% through 2027.

There are early indications that liquidity, policy, and sentiment are aligning in a way that could create a more constructive backdrop than in recent years. With households starting to rotate, foreign funds re-engaging, insurers underwriting equity demand, IPOs reopening as a fundraising path, and early signs of corporate improvement, the foundations for a broader rally are forming.

The question now is not whether China can rally, but whether this marks the beginning of a more durable cycle.

Gold Rush?

[Drag image to zoom in]

Gold did it again. With a remarkable rally of 47% year to date, prices continue to make successive highs and making its best year since the 1970s. What looked like a panic spike now reads as a broad reinforcement of gold’s role as a macro hedge against policy, geopolitical and real yield risks. The move remains anchored by central banks increasing allocations and by China’s sustained pivot towards gold reserves.

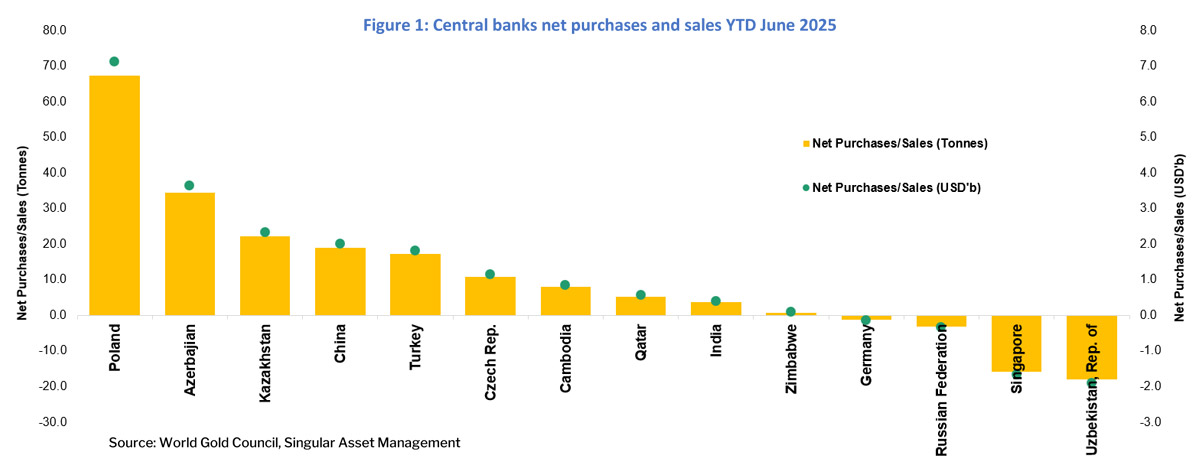

Extending further from our March 2025 report, demand from central banks remained the central pillar in the precious metal’s ascent to record highs. As of July 2025, based on data from the World Gold Council, global central banks were still net buyers in 2Q25. Gold’s share of reported foreign reserves rose to 21.7% (+4.8ppt YoY; +0.5ppt QoQ). Buying in 1H25 was led by emerging markets diversifying away from concentrated dollar holdings, with top additions from Poland (67.1t), Azerbaijan (34.5t), Turkey (31.2t), Kazakhstan (24.7t), and China (20.8t) (Figure 1). While purchase motivations are multifactorial, the prominence of buyers in countries proximate to Russia is hard to ignore, a sign that related geopolitical risk plays an important part in the demand story.

China is the second distinct engine. Despite close market scrutiny, they have extended its buying streak to ten consecutive months, strengthening China’s standing in the global bullion market. Currently ranked 6th globally by official holdings, they are also exploring a role as custodian for foreign sovereign gold reserves, within the Shanghai Gold Exchange (“SGE”) International Board ecosystem under The People’s Bank of China (“PBOC”), which would bolster its position as a steady buyer and holder of gold. In parallel, China continues to open its gold market by easing import restrictions and launching its first offshore vault and contracts in Hong Kong to attract transaction volumes—making Chinese vaults an increasingly attractive option for building reserves.

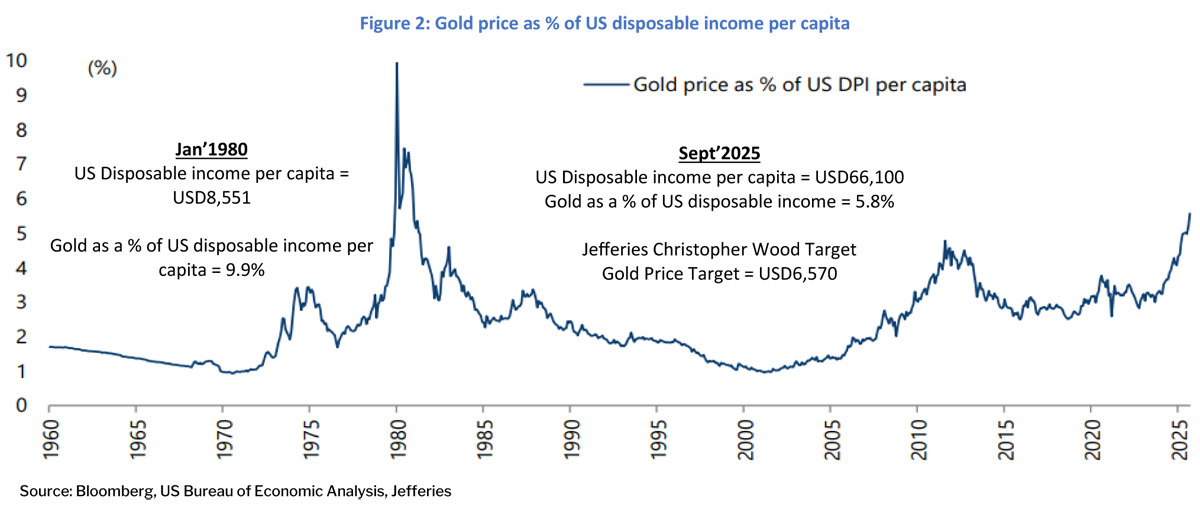

Even at current price levels for gold, Street bias remains constructive. Jefferies’ Christopher Wood frames a long-run anchor by benchmarking gold to US disposable personal income (“DPI”) per capita. Compared to the previous 1980 secular bull market, gold equated to 9.9% of DPI per capita, versus roughly 5.8% today. Applying that heuristic to today’s DPI per capita of US$66,100; 7.7x higher than in the 1980, it implies a cycle-peak price target of around US$6,570/oz for gold (Figure 2). Separately, Goldman Sachs reiterates gold as its highest-conviction long in commodities, sketching US$5,000/oz if just 1% of privately held U.S. Treasuries were to rotate into bullion. These are scenarios, not base cases, but they capture the asymmetry while central banks keep buying and market plumbing improves.

[Drag image to zoom in]

After an almost uninterrupted climb since early 2024, while persistent policy risk and ongoing central-banks demand can keep the bid intact, any meaningful rise in real yields and visible trimming by major holders could equally cool the tape. Although sentiment remains firmly bullish, it does not necessitate that the path will be linear. Ultimately, only time will tell which way gold’s next chapter breaks.

From Typhoon to Takeaways - On the Ground in Hong Kong

Source: Singular Asset Management

Talent was another recurring theme. Analysts described a wave of PhD-level hires into analyst and research roles, with many relocating from mainland China into Hong Kong — deepening the city’s talent pool but also pushing up residential rents. This hiring momentum fits into a broader backdrop: Hong Kong has risen from 9th to 4th in the World Talent Ranking, while China is projected to produce nearly twice as many STEM PhD graduates as the US in 2025. Together, these trends underline the long-term human capital advantages supporting China’s innovation agenda.

Another takeaway was the clear pivot of many Chinese corporates toward profitability over sheer market share expansion, signaling a more disciplined competitive environment. This narrative resonated with investors seeking sustainable returns. Innovation was also on display. Demonstrations such as AR glasses with real-time translation, teleprompting, and camera integration showed how quickly technologies are moving from concept to practical application. Despite the headwinds facing regional economies, the tone at the conference reflected rising optimism. Both corporates and investors appeared aligned in their outlook, signaling confidence that Hong Kong and China markets remain resilient and well-positioned to capture future growth.

Malaysia Market Review

Cashing In on Resilience

That resilience is also beginning to filter into equities. September brought breadth to a market (See Figure 1) long weighed down by sluggishness. The benchmark (FBM KLCI) gained 2.3%, while the smaller, more volatile ACE Market surged nearly 10%, trimming their year-to-date losses to 1.9% and 3.9% respectively.

[Drag image to zoom in]

[Drag image to zoom in]

Part of the new optimism comes from real money flowing onshore. In the auto space, BYD has recently secured 150 acres within the 1,500-acre TechPark master plan in Tanjong Malim, in a deal analysts value at roughly RM98 million (RM15 psf), with assembly lines slated to start in 2026. In Hulu Selangor, Chery has gone bigger, committing RM2.2 billion to a 200-acre smart auto park—Phase 1 of an ~800-acre master development.

The influx of foreign capital isn’t confined to the autos. Our channel checks point to Chinese private education groups making inroads into Malaysia’s education market, extending their global footprint through acquisitions of local higher education institutions.

For instance, Shandong’s Weifang Institute of Technology have acquired a 70% stake in Nilai University, positioning it as a springboard to capture steady demand from Chinese students, who already make up a large share of Malaysia’s foreign enrolments. Similarly, Infrastructure University Kuala Lumpur, recently rebranded as KLUST (Kuala Lumpur University of Science & Technology), was also acquired by Star Teenagers International, which purchased a 90% stake for RM27 million.

Certainly, Chinese investors’ interest in Malaysia is gaining traction. That sentiment was shared on the ground when we engaged with students in the Executive Master of Business Administration (EMBA) program, most of whom are senior decision-makers from leading companies and established entrepreneurs.

[Drag image to zoom in]

Aside from FDI, Malaysia has been firing on all cylinders to boost tourism, setting an ambitious target of 47 million international visitors (36 million excluding excursionists; up 44% from 25 million in 2024) and a record-high MYR147.1 billion in receipts for Visit Malaysia Year 2026.

Not surprisingly, China ranks among the top three sources of tourist arrivals, with 3.3 million travellers. This momentum continues to build with Malaysia gaining Chinese market share from other competing ASEAN destinations.

Turning to the domestic front, consumption is set to strengthen, buoyed by clarity on the RON95 targeted subsidy scheme and the rapid uptake of the RM2 billion SARA cash aid—where 11.8 million recipients spent RM745 million within just a week of its launch.

Beyond policy clarity and cash transfers, Bank Negara’s 25 bps rate cut could provide a further lift. With total outstanding loans at RM2.3 trillion, the move equates to RM5.8 billion in annual interest savings—RM3.8 billion for households and RM2.1 billion for businesses.

For households, that means smaller mortgage or car loan repayments; for corporates, leaner financing costs that free up cash for expansion. Put simply, more disposable income and stronger balance sheets could translate into higher spending and investment.

中国股市反弹:才刚开始,能否持续?

[Drag image to zoom in]

利率下行是重要背景。一年期银行存款利率目前已降至1%以下,创下历史新低,迫使家庭考虑其他投资选择。在现金回报率被压缩的情况下,股票在“寻求收益”的过程中更具吸引力。

在国内,国有背景机构正发挥着市场支撑作用。作为中国投资公司一部分的中央汇金已累计持有约1800亿美元的ETF,随着市场反弹而实现了可观的账面收益。大型保险公司则被要求将30%的新保费配置至股票,为机构资金需求提供了稳定基础。

外资也在回流。彭博社近日报道称,中国正在摆脱“不具投资价值”的标签,全球资金自2021年以来首次重新进入多个资产类别。对冲基金在A股市场尤为活跃,而长期投资者也开始逐步加仓。同时,香港IPO市场的兴趣复苏,为国际资本进入中国提供了新的渠道。

尽管国内与区域基金更快地转向中国和香港股市,全球投资者的回归仍未全面展开。持仓数据显示,今年以来,亚洲和新兴市场导向的基金持续增加对中国的配置,而全球主动型基金相较基准仍维持低配。这一差距凸显近期行情主要由区域资金推动,若全球资金更坚定回归,仍有进一步上涨空间。

在香港,IPO募资正呈现复苏迹象。2025年上半年,共有42只新股上市,筹资1071亿港元,同比大增逾700%。平均上市后表现也为正,帮助恢复了对香港作为全球资本进入中国门户的信心。

企业基本面在部分领域也出现改善迹象。产能利用率与平均售价正在上升,受益于北京推动的“反内卷”政策,鼓励更理性的竞争。上市公司上半年盈利有所改善,市场一致预期今年实现中个位数增长,并在2027年前保持约9%的年均复合增长率。

流动性、政策与市场情绪正在逐步形成合力,这可能营造出比近年来更为积极的市场环境。随着家庭资金开始转向、外资回流、保险资金托底股市需求、IPO重新开启募资渠道,以及企业端初步改善迹象出现,更广泛的上涨行情基础正在形成。

现在的问题不在于中国能否迎来反弹,而在于这是否标志着一个更持久周期的开始。

淘金热?

[Drag image to zoom in]

黄金又一次创造纪录。年初至今大涨47%,价格不断刷新新高,创下自1970年代以来最佳年度表现。原本看似恐慌性的急涨,如今已被视为黄金作为宏观对冲工具的广泛强化,其作用在于抵御政策风险、地缘政治风险以及实际收益率风险。这一趋势依然受到央行增持配置以及中国持续转向黄金储备的推动。

在我们2025年3月的报告基础上,央行需求仍是推动贵金属创下历史新高的核心支柱。根据世界黄金协会的数据,截至2025年7月,全球央行在2025年第二季度仍为净买入方。黄金在已披露外汇储备中的占比升至21.7%(同比+4.8个百分点;环比+0.5个百分点)。2025年上半年买入主力来自新兴市场国家,借此分散对美元的高度集中持有,增持最多的包括波兰(67.1吨)、阿塞拜疆(34.5吨)、土耳其(31.2吨)、哈萨克斯坦(24.7吨)以及中国(20.8吨)(见图表1)。虽然购买动因多元,但这些买家大多地处俄罗斯周边,凸显相关地缘风险在需求故事中扮演的重要角色。

中国则是另一大引擎。尽管市场高度关注,中国已连续10个月延续购金热潮,巩固了其在全球黄金市场的地位。目前官方持有量全球排名第六,同时也在探索在上海黄金交易所(国际板)体系下,人民银行作为外国主权黄金储备托管方的可能性,这将进一步加强其作为稳定买家和持有者的角色。与此同时,中国也在持续对外开放黄金市场,放宽进口限制,并在香港设立首个境外金库及相关合约,以吸引更多交易量,使中国金库成为越来越具吸引力的储备建设选择。

即便在当前的金价水平,市场主流观点依然乐观。Jefferies的Christopher Wood以美国人均可支配收入(DPI)为基准,构建了黄金的长期锚定指标。与1980年上一轮长期牛市相比,当时黄金价值相当于人均DPI的9.9%,而目前仅约5.8%。以当下人均DPI 66,100美元为基础(是1980年的7.7倍),对应的周期峰值金价约为每盎司6,570美元(见图表2)。另一方面,高盛继续将黄金列为其最坚定的商品多头,预测若仅1%的美国私人持有国债转向黄金,金价即可达到每盎司5,000美元。这些情景虽非基准预测,但很好地展示了当央行持续买入、市场机制改善时的上行不对称性。

[Drag image to zoom in]

自2024年初以来黄金几乎持续上行。虽然政策风险的延续和央行需求的持续能够维持买盘,但若实际收益率显著上升,或主要持有方出现明显减仓,也可能令金价降温。尽管市场情绪依旧强烈看多,但并不意味着未来走势会是一条直线。最终,黄金的下一个篇章将走向何方,唯有时间能够揭晓。

从台风到启示——香港实地观察

Source: Singular Asset Management

人才同样是反复出现的主题。分析师提到,大量博士级人才涌入分析与研究岗位,许多人从中国内地迁往香港——这不仅加深了香港的人才库,也推高了住宅租金。这一招聘趋势契合更广泛的背景:香港在全球人才排名中已从第9位上升至第4位,而预计到2025年,中国STEM博士毕业生人数将接近美国的两倍。这些趋势共同凸显了中国在人力资本方面的长期优势,为其创新议程提供支撑。

另一大收获是,许多中国企业已明显从单纯追求市场份额转向更注重盈利能力,显示出更具纪律性的竞争环境。这一转变引发了寻求可持续回报的投资者共鸣。会议上还展示了创新成果,例如具备实时翻译、提词和摄像功能的增强现实眼镜,显示出科技正迅速从概念走向实际应用。尽管区域经济仍面临逆风,但会议氛围反映出乐观情绪不断上升。无论是企业还是投资者,都展现出趋同的前景预期,传递出香港和中国市场仍具韧性,并已做好把握未来增长机遇的信心。

马来西亚市场回顾

把握韧性,兑现回报

这种韧性也开始传导至股市。9月,长期受低迷拖累的市场迎来广度回升(见图1)。基准指数FBM KLCI上涨2.3%,而规模较小、波动更大的ACE市场飙升近10%,将年初至今的跌幅分别收窄至1.9%和3.9%。

[Drag image to zoom in]

[Drag image to zoom in]

新的乐观部分来自真实资金的流入。在汽车领域,比亚迪近期在丹戎马林的1,500英亩科技园总体规划内获得150英亩土地,交易估值约9,800万令吉(每平方英尺15令吉),计划于2026年启动组装线。在乌鲁雪兰莪,奇瑞投入更大,承诺22亿令吉开发一个200英亩的智能汽车园区——这是约800英亩总体开发的第一阶段。

外资流入不仅限于汽车。我们的渠道调查显示,中国民办教育集团正进入马来西亚教育市场,通过收购本地高等教育机构扩展其全球版图。

例如,山东潍坊学院已收购汝来大学70%股权,将其定位为承接中国学生稳定需求的跳板——中国学生已占马来西亚外国留学生的大部分。同样,吉隆坡基建大学(现更名为吉隆坡科技大学 KLUST)也被星辰国际收购90%股权,交易金额2,700万令吉。

可以肯定的是,中国投资者对马来西亚的兴趣正在升温。我们在与高级工商管理硕士(EMBA)项目学生交流时也感受到这一点,他们大多是知名企业的高层决策者或成功企业家。

[Drag image to zoom in]

除外资之外,马来西亚在推动旅游业方面全面发力,设定了一个雄心勃勃的目标:2026马来西亚旅游年吸引4,700万国际游客(若不计短途游客则为3,600万,较2024年的2,500万增长44%),并实现1,471亿令吉的创纪录收入。

毫不意外,中国位列三大游客来源国之一,达到330万人次。随着马来西亚从其他竞争性的东盟目的地中赢得更多中国游客市场份额,这一势头仍在增强。

回到国内层面,消费有望走强,受益于RON95汽油目标补贴方案的明朗化,以及20亿令吉SARA现金援助的快速消耗——1,180万受益人在启动后一周内就花费了7.45亿令吉。

除了政策明晰和现金转移外,马来西亚国家银行25个基点的降息也可能带来进一步提振。按总贷款余额2.3万亿令吉计算,此举相当于每年节省58亿令吉利息支出——其中38亿令吉属于家庭,21亿令吉属于企业。

对家庭而言,这意味着更低的房贷或车贷月供;对企业而言,则意味着融资成本降低,释放更多现金用于扩张。简而言之,更高的可支配收入和更健康的资产负债表,有望转化为更强劲的消费与投资。